Email: laurie.e.page@lpl.com

CALL NOW! (941) 932-4822

Blog

In 2022, banks saw an 84% increase in check fraud

What to do if you get really lucky

Getting involved with community organizations and charities can help you, as well as others

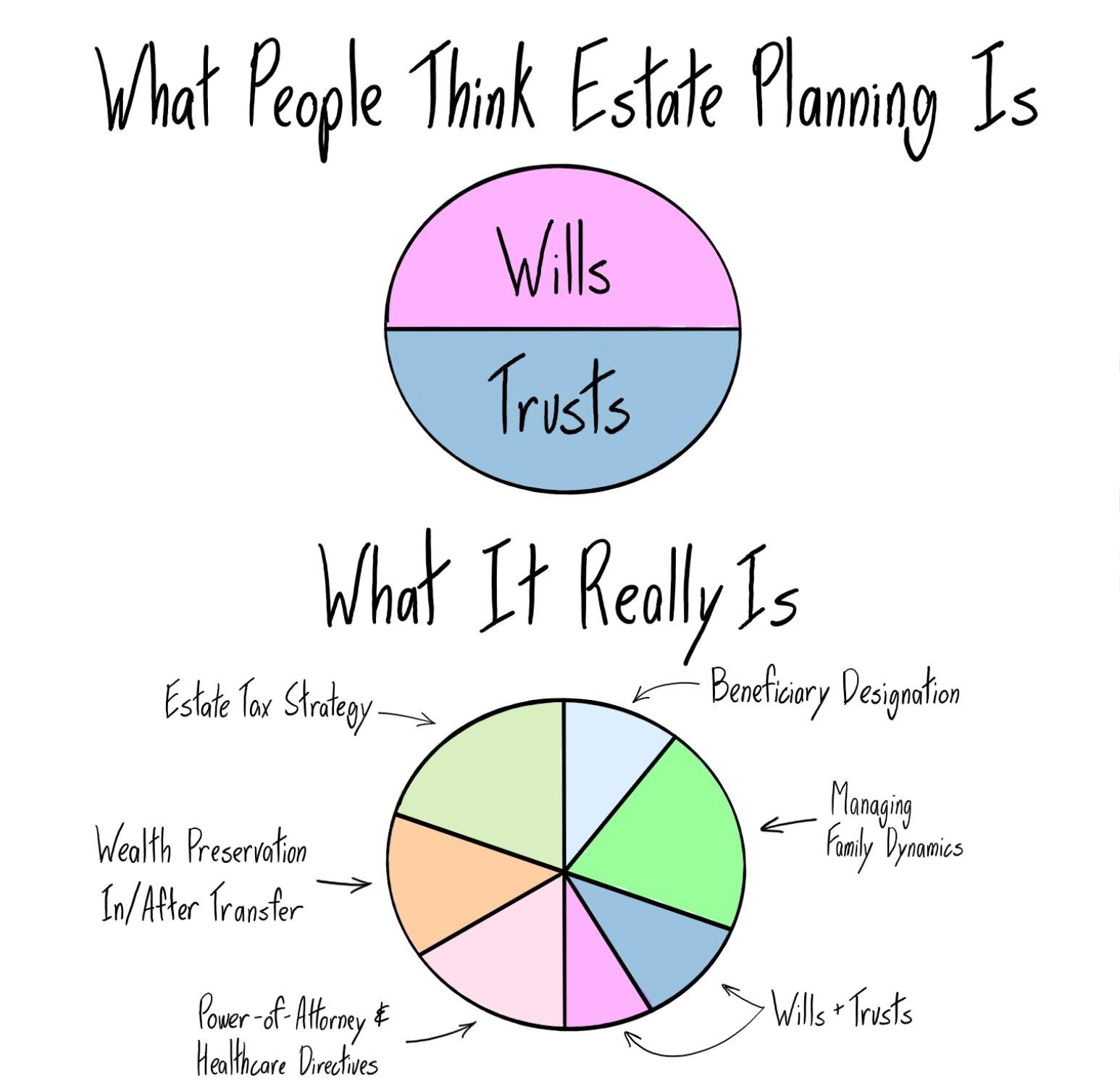

Putting it off and dying "intestate" may not be the legacy you want to leave your loved ones

It’s interesting how personal events can provide some of the best inspiration. My grandmother passed a couple of weeks ago, and as my family was making her final arrangements, and I experienced the emotions that my own family was feeling, it occurred to me that these are things that families experience every day. And while I was providing council to my own family, I thought, why not provide similar council on a larger scale to help lift some of the weight from the shoulders of families at large? So, let’s talk about final expense planning. The big question here is how will your final expenses be paid? There are a few main options: proceeds of your financial accounts, life insurance and pre-need arrangements. Each of these options have a few considerations to keep in mind, so let’s dig a little deeper. First, proceeds from your financial accounts. A common misnomer is that your Power of Attorney can continue to conduct business on your behalf even after your passing. This is false. Your Power of Attorney expires when you expire. Ergo, when you pass, all your financial accounts will be frozen until such time that proper estate claims can be filed and processed. This can be simplified and expedited by properly naming beneficiaries on your accounts and keeping them current but be aware that there will still be some processing time involved before your next of kin will receive the proceeds of your accounts and have access to the funds that are left to them. Next, let’s look at life insurance. This is very commonly thought of as the go-to solution for final expenses, however, life insurance often poses an even bigger liquidity issue than using proceeds from your financial accounts. To file the claim with the life insurance company, you will need to obtain a certified copy of the death certificate, which can sometimes take some time and expense to procure. Most life insurance companies still require an original copy of the certified death certificate as part of the claim, which will require you to mail the copy to them via regular mail. Once the insurance company receives the original, certified copy of the death certificate, claims processing can take several weeks before your beneficiaries receive the proceeds of your policy. While life insurance is a great way to provide an income tax free benefit to your heirs, it is often used more effectively in other areas of financial planning, such as survivor income, and business buy-sell agreements than it is in final expense planning due to the delayed liquidity. So, if not proceeds from financial accounts or life insurance, how are you to provide assets for your loved ones to pay for your final expenses? Enter pre-need arrangements. Pre-need arrangements come in a couple of different forms. First, let’s talk about the option that my grandmother chose many years ago. My grandmother purchased a pre-paid funeral annuity from the local funeral home. This is a good option because it guarantees that your final expenses are paid through assets that cannot be penetrated by Medicaid. There is one thing that it misses, though. No decisions are made. I watched my dad, uncle, and aunt struggle with decisions of “what would mom have wanted?” and “I don’t even know her favorite color, favorite flower or favorite song” when all there was at the funeral home was a pool of money to spend as they guessed their way through their mother’s final farewell. So, what’s the other choice? You also have the option to fully pre-plan your arrangements – everything from traditional burial vs. cremation, to the color scheme, to the flowers, to the music, to any religious traditions that you do or do not want to include. Furthermore, these arrangements are paid in today’s dollars, potentially leaving a greater percentage of assets in your estate should inflation raise prices at the time of your passing. Additionally, since this option is also fully pre-paid, you don’t need to worry about Medicaid penetrating these assets, should that need arise for your financial situation. Lastly, it provides you assurance that your final wishes will be honored. Personally, I can tell you, for myself, there are probably 2 people in the world that know my favorite color, flower and song and based on human life expectancies, it is more likely that I will be making their arrangements than that they will be making mine. What a wonderful final gift to give to those you love – to ease their burden in their time of grief by taking away any question of what you would have wanted. For more information on final expense planning or any financial planning concerns, please feel welcome to reach out to the advisory team at Sound Wealth Management at 941.932.4822 or schedule your no obligation consultation online at www.soundwealth.net . It’s time for you to be heard!

The experience often benefits both mentors and mentees -- and their organizations

Women face more financial roadblocks, and strive harder to overcome them

The pros and cons of pooling finances with your significant other

A divorce can have a profound impact on your finances. We outline key considerations for maintaining your financial health as you proceed through the process. No matter whether your divorce is amicable or contentious, it can have a profound impact on your finances. There are myriad rules and regulations to consider. We outline some of the most significant and how they could impact your assets. Who Gets What No matter where you reside, generally any assets or property that you acquired while married will be divided when you divorce. There are a few exceptions. For instance, if you inherited assets or received gifts individually, the division rule may not apply. Also, you may be able to keep the assets and property that you acquired before you got married. However, your state law will set out how to divide your assets and property, and it will follow one of two routes: 1. Common law property states include those states where the judge has discretion to listen to individual circumstances before dividing assets and property. Those factors include: earning ability for each spouse; the duration of the marriage; and the amount that each spouse contributed to building the marriage’s assets. All but nine states follow this format. 2. Community property states, on the other hand, are those in which courts generally equally divide assets and property acquired during the marriage. The states that observe this law are: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. [1] In addition, residents of Alaska can choose to opt in to a community property agreement. [2] What About Debt? Debt survives a divorce, and states differ as to how they allocate which spouse is responsible for which debt. 1. Common law states (see above) assign debt acquired in individual accounts to the account holder, while debt in joint accounts is generally treated the same way as assets and property. 2. Community property states typically divide debt equally between spouses, no matter whether it was from an individual or joint account. You should close all joint accounts post-divorce to avoid being responsible for debts that your spouse incurs. Once the divorce is finalized, have them reclassified as individual accounts by your creditors. If you and your spouse have a mortgage for a home that has appreciated in value, consider selling it before the divorce is finalized, as the IRS allows you to take advantage of $500,000 in realized capital gains if you are a married taxpayer, an amount that is cut in half for single filers. We recommend consulting a tax advisor to navigate these rules. Retirement Assets If you or your spouse have money in a 401(k) or pension plan, it may also be divided during a divorce. You can seek a share of your spouse’s 401(k) or pension plan benefit if you obtain a Qualified Domestic Relations Order (QDRO) and present it to your spouse’s plan sponsor before distributions have been completed. If your efforts are successful, you may decide to roll them over into an IRA to defer taxes. Discuss this option with a financial professional who is familiar with the divorce process. Estate Planning If you have already drafted a will, make sure that you review it (and if you don’t have one, work with an estate planning attorney to draw one up). The attorney will work within your state’s estate laws to distribute your assets properly. Review your beneficiary designations for any pensions, 401(k)s, and insurance policies. Note that a spouse is required under federal law to be the sole beneficiary of pension and 401(k) benefits unless that spouse waives such rights. With so much at stake financially as you proceed through a divorce, don’t do it alone; it’s best to work with an attorney or financial professional who specializes in the process to help protect your assets to the greatest extent possible. [1] Business Insider, Updated Nov 29, 2022: In 9 US states, a divorce could mean losing half of everything you own [2] FindLaw: Alaska Marital Property Laws This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. This material was prepared by LPL Financial, LLC. Member FINRA/SIPC

Credit card usage is ubiquitous for Americans. Online purchases are just a click away when paying with a card, while other transactions — car rentals, for instance — require a credit card for both payment and security. Commensurate with credit card usage is carryover debt that accumulates each month, a financial strain for those entering retirement. There are a few key considerations for using a credit card once you’re relying on a fixed monthly income. When living on a fixed income, using a credit card as if it is actually income may deliver a short-term benefit — i.e., that big ticket item that looked too good to pass up. However, it comes at a long-term cost: an inability to sustain your standard of living. Paying for groceries and other necessities may seem convenient with just a swipe or tap at the register. But, unless you can pay off the balance each month, you’ll incur a credit card bill that accumulates finance charges each month, making it an increasingly formidable debt to discharge. What to Consider When Selecting a Credit Card Not all credit cards are alike. When assessing whether to sign up for a card, consider your intended use. Cards with enticing rewards programs may be appropriate if you’re paying off the balance each month, though these programs typically come with hefty annual fees. Also, if the cards include a high interest rate, it’s financially prudent to turn down the potential rewards and instead look for a card with a lower interest rate. Nurture Your Credit You can receive a lower interest rate on a credit card if your credit score is strong. To improve your rating, pay your bills on time and minimize your debt. Chipping Away at Debt While doing away with all credit cards may be impractical, reducing your debt will help keep your finances in order and your fixed income more predictable. This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. This material was prepared by LPL Financial, LLC. Member FINRA/SIPC